Tariff Whiplash and the Market’s Rising Uncertainty Premium

February 23rd, 2026

Over the past several days, trade policy has moved quickly and dramatically. A Supreme Court ruling declared prior tariffs unconstitutional. Within days, the executive branch announced a 10% global tariff under Section 122 authority — and shortly thereafter raised that figure to 15%. At the same time, discussion has emerged that previously collected tariff revenues might need to be refunded.

Markets are being asked to price rapidly shifting policy decisions. Volatility is increasing and the premium to hold risk is rising.

Regardless of one’s political view, this sequence matters for markets.

When the legal status, size, and permanence of tariffs can change within days, businesses face planning uncertainty. Investors must then price not just economic impact, but policy unpredictability.

This week’s market behavior reflects that shift.

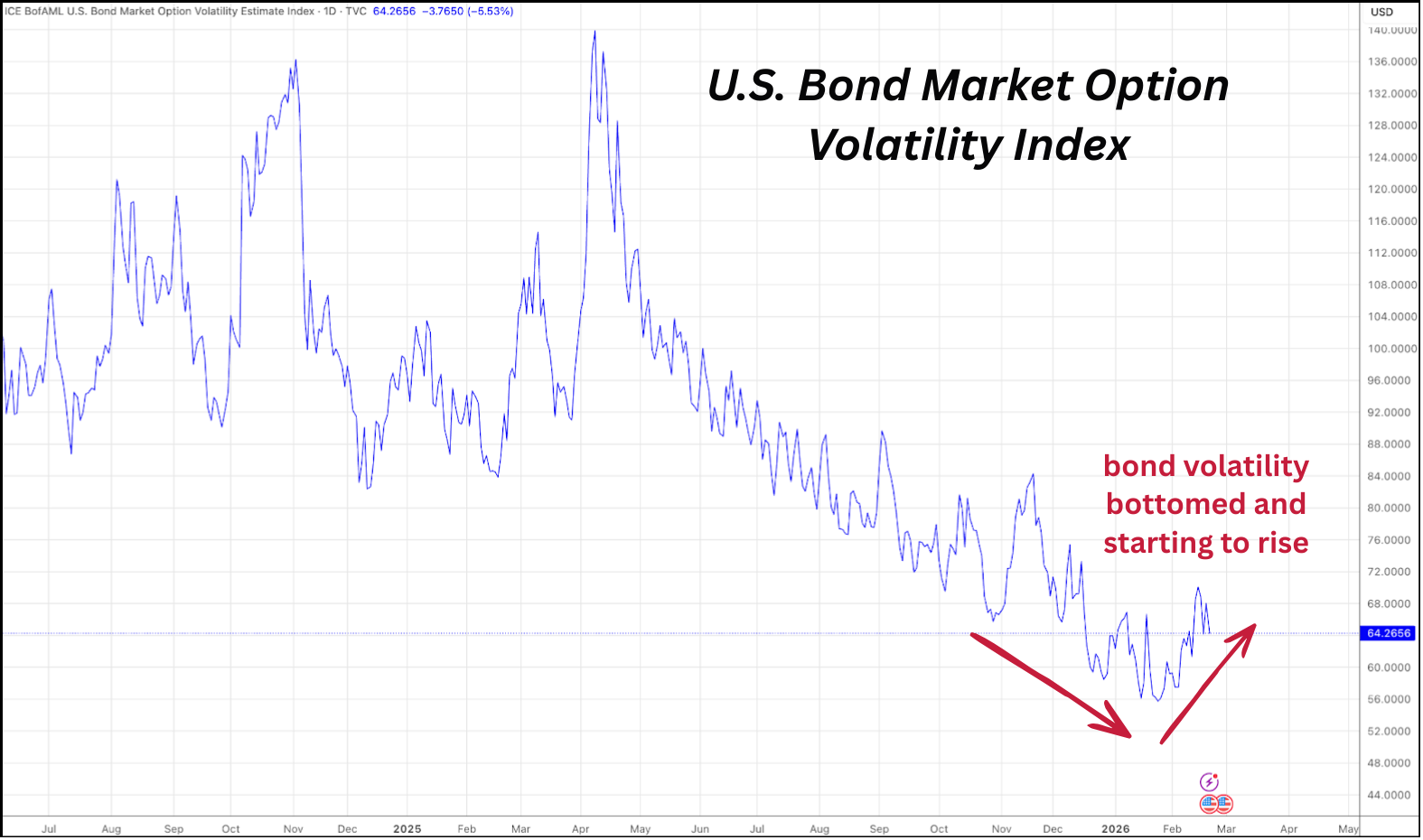

Volatility Is Being Priced More Explicitly

Bottom Line

Uncertainty is no longer episodic — it is being embedded in bond markets.

The MOVE index, a measure of bond market volatility, has risen over the past month. At the same time, the 10-year Treasury yield has fallen by approximately 16 basis points.

Falling yields typically signal growth concerns or defensive positioning. Rising bond volatility signals something different: uncertainty about the policy path itself.

When yields fall but volatility rises, it suggests markets are repositioning while remaining unsure about the stability of the forward trajectory.

That dynamic is consistent with a higher volatility premium.

Defensive Rotation Is Emerging

Bottom Line

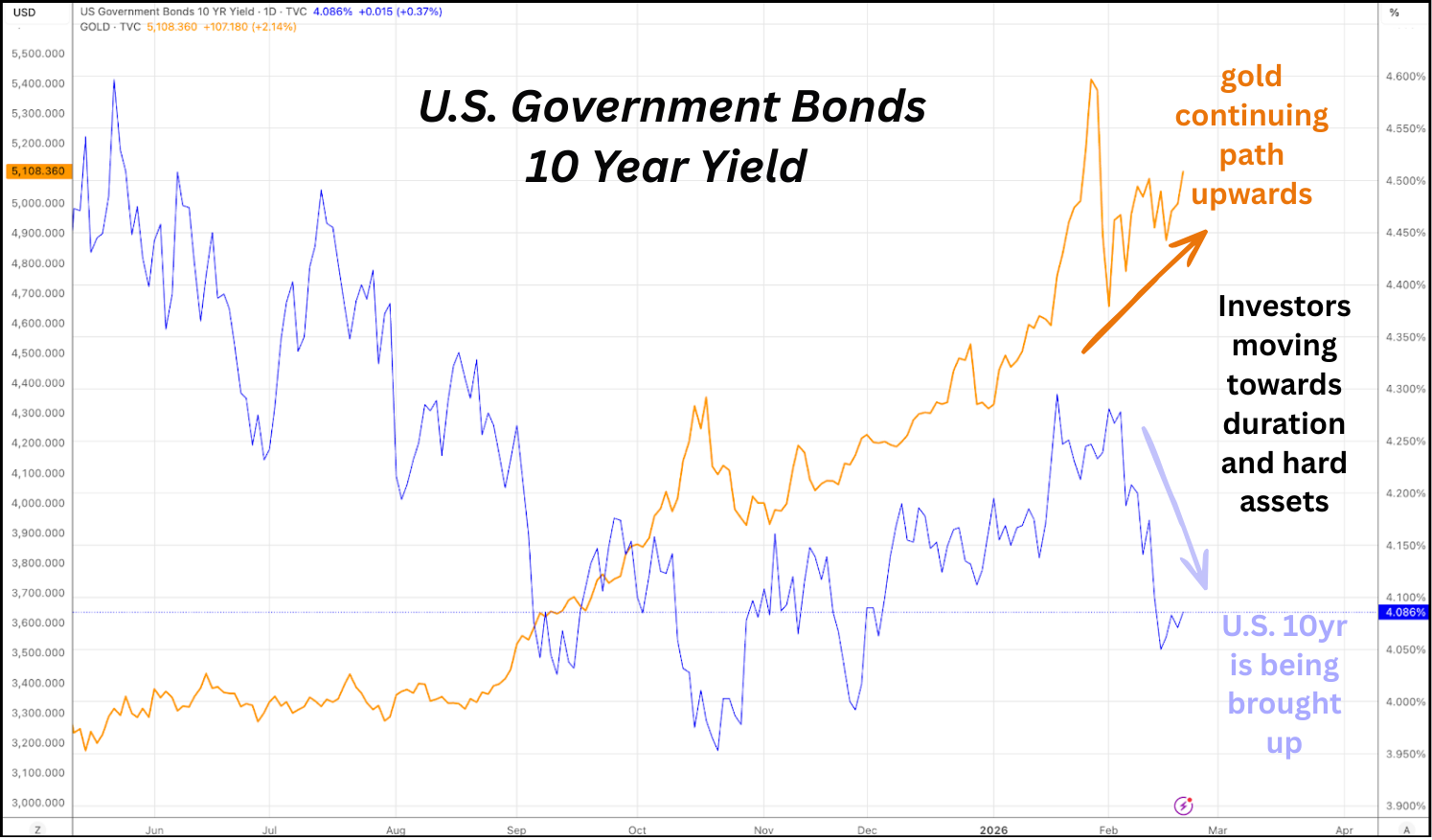

Capital is rotating toward duration and hard value rather than exiting the system altogether.

Over the past 30 days:

Gold is up nearly 6% - hard assets being bought up

The 10-year yield has declined - duration being bought up

This is not liquidation behavior. It is repositioning.

Investors appear to be trimming exposure to more speculative areas while adding exposure to assets traditionally viewed as more durable under uncertainty — duration and hard value.

Gold, in particular, continues to act as a hedge against fiat and policy instability rather than a signal of systemic panic.

Risk Appetite Is Narrowing - Not Fully Breaking

Bottom Line

The more speculative corners of the market continue to weaken, but broad participation remains steady.

Bitcoin has declined roughly 23% over the past 30 days and remains near recent lows. Meanwhile, the S&P 500 index itself is largely unchanged over the same period. The percentage of S&P 500 stocks trading above their 200-day moving average currently sits near 67% - roughly where it stood a month ago.

That tells us something important. Participation has not collapsed. Breadth has not deteriorated meaningfully. Credit markets remain orderly.

This is not systemic collapse, it is selective compression - the trimming of speculative risk at the edges while the core remains comparatively steady.

Bringing It all Together

The system’s piping appears steady for now — but uncertainty is increasing, and volatility premiums are rising accordingly.

The market is digesting three simultaneous forces:

Rapidly shifting trade policy and legal uncertainty.

Defensive capital rotation toward duration and gold.

Continued compression in speculative assets.

So far, financial plumbing is holding. Credit is stable. Equity breadth is steady. There are no clear signs of broad disorder. But markets are demanding greater compensation for uncertainty. That distinction matters.

Risk is not being abandoned completely. It is being repriced more carefully.

What We’re Watching Next

Does bond volatility continue rising even if yields stabilize?

Does equity breadth begin to deteriorate meaningfully from current levels?

Does policy messaging stabilize — or continue shifting rapidly?

The answers to those questions will determine whether this remains a controlled rotation — or evolves into something more consequential.

For now, the adjustment appears disciplined.

But the volatility premium is no longer negligible.

Markets are not repricing at random. What we are witnessing is a coordinated adjustment across currencies, assets, and sectors as leverage is worked down through revaluation.

USD easing plays a central role in this process, allowing real assets to reprice without destabilizing balance sheets. Sector behavior — from real estate to health care to emerging markets — reflects this same mechanism expressing itself in different forms.

This deleveraging process is likely to be long and uneven. Periods of calm may persist, but they coexist with the potential for sharp, discrete repricing steps as constraints are reached and pressure is released.

Understanding the mechanism, rather than reacting to headlines, remains the key to navigating what lies ahead.

Look out for next week’s newsletter for further insight into the forces shaping today’s markets.